PETALING JAYA: The resilience of the banking sector will be put to test in the second half of the year as economic conditions remain weak with no signs of the coronavirus disease (Covid-19) abating.

The three main obstacles in its path are the compression in net interest margin (NIM) from the low overnight policy rate (OPR) which could potentially decline further towards the end of the year, higher levels of non-performing loans (NPLs) and lower lending activities.

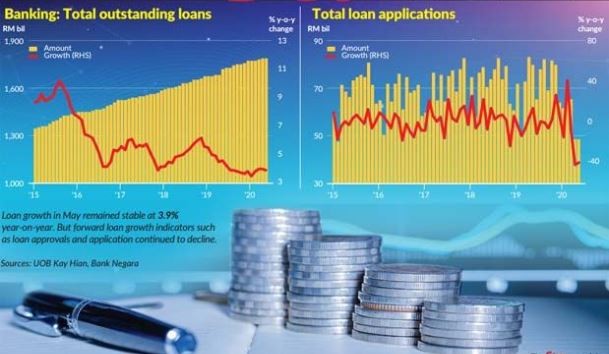

The banks’ main business is lending and the latest leading loan growth indicators as of May do not look too good, signalling lacklustre loan growth this year.

In May, loan applications fell 39% year-on-year (y-o-y) while total loans approved sank 54.4% y-o-y.

Application for consumer loans fell 58.5% y-o-y as consumers were not spending on big ticket items such as houses and vehicles while business loan applications were down 13.9%.

While the system loan growth remained stable with only a marginal slip to a growth of 3.9% in May as compared to 4% in April, Maybank IB Research pointed out that the hefty contraction in loan applications puts further pressure on loan growth.

CGS-CIMB Research said loan growth was stable because the 25.8% y-o-y drop in loan disbursement in May was largely offset by a 22.3% decline in loan repayment due to the moratorium.

Out of the 3.9% loan growth, UOB Kay Hian Research said, business loan growth moderated to 4.9% y-o-y on the back of slower working capital loan growth while household loan growth softened to 3.2% y-o-y due to slower residential property loan growth.

The research house expected loan growth to taper off to 2.8% for the whole of 2020 on the back of slower demand for large ticket items and weak business sentiment.

“Our assumption takes into account the partial effect from the temporary spike in initial working capital needs during the early phases of the lockdown and lower repayment during the six-month automatic moratorium on consumer as well as small and medium enterprise (SME) loans.

“Note that Malaysia is the only country that has an automatic loan moratorium on consumer and SME loans, which could artificially suppress NPL and consequently credit cost trends over the next six months, ” it said in a research note.

Meanwhile, fixed deposits have also contracted for the third consecutive month to RM984.3bil in May but the current account and savings account (Casa) on the other hand, grew at a faster pace in May at 13.7% y-o-y as compared with12.6% in April.

MIDF Research senior analyst Imran Yassin Yusof (pic below) told StarBiz that the market can expect new loans growth to be muted and while this would impact the interest income of the banks, the lower interest expense with the contraction in fixed deposits (FDs) will come in to cushion the net interest income compression.

He expected the trend to continue up to 3Q20 as a cautious climate still prevailed.

Asked if the drop in loan applications and approvals were due to banks being conservative or Malaysians were not spending, Imran said it could be both but it was difficult to pinpoint the actual scenario.

“It could be a combination of a conservative stance from the banks to protect their asset quality and also less demand for loans given that consumers will likely hold back on discretionary spending.

“However, we have seen some improvement in terms of property and auto purchases in June and this may lead to better overall statistics in June.

“The question is whether this is sustainable, which we believe may not be so given the pronounced economic impact of Covid-19 and the movement control order, ” he said, adding that the research house expected the situation to improve in 4Q20 as the economy starts to rebound.

Imran also said in a research note yesterday that the drop in FDs and surge in Casa suggested that depositors were reluctant to tie-up their cash flows and wanted to have sufficient liquidity given the uncertain conditions of Covid-19.

Maybank IB viewed this as something positive for banks in their ability to manage funding cost and improve margins.

An analyst said banks are stuck in a situation where they want to be pushing out more loans in this low interest rate environment but no one is borrowing.

And when banks go for riskier customers in exchange for higher returns, they take on the risk of potentially higher NPLs and provisions.

“As a matter of prudence, the MFRS 9 requires banks to make provisions when there is a significant increase in credit risk of their borrowers and this will impact the banks’ earnings.

“There are a lot of constraints for banks in this economic environment. Banks are also facing further compression in NIM should the OPR be reduced further, ” he said.

The OPR has seen three cuts this year to a 10-year low of 2%.

Analysts have mixed views over the upcoming monetary policy committee meeting on July 7, with some predicting that the rate will remain while others projected up to 50 basis points being slashed.

Source: https://www.thestar.com.my/business/business-news/2020/07/02/mild-loan-growth